Blog

Insurance Claims for Commercial Roof Damage: Documentation and Process Guide for LA Property Owners

June 16, 2026

Insurance Claims for Commercial Roof Damage: Documentation and Process Guide for LA Property Owners

When your commercial property in Southern California suffers roof damage, navigating the insurance claims process can feel overwhelming - especially when you’re managing compliance requirements for healthcare facilities or other regulated industries. Understanding how commercial roof insurance claims work, what documentation insurers require, and realistic timelines can mean the difference between a smooth claim resolution and months of delays that impact your operations.

Property managers and facilities directors across Los Angeles County face unique challenges when dealing with roof damage claims. From documenting storm damage on flat warehouse roofs to coordinating with adjusters while maintaining operational continuity, the process requires strategic planning and thorough preparation. This guide walks you through the essential steps to maximize your claim success while minimizing business disruption.

Understanding Commercial Roof Insurance Coverage in California

Commercial property insurance policies vary significantly in their roof damage coverage, and understanding your specific policy terms is crucial before damage occurs. Most commercial policies in California fall into three main categories: replacement cost coverage, actual cash value, and functional replacement cost.

Replacement cost coverage pays to repair or replace damaged roof sections with materials of like kind and quality, without depreciation deductions. This typically provides the most comprehensive protection for commercial property owners, though premiums reflect this enhanced coverage.

Actual cash value policies factor in depreciation based on the roof’s age and condition at the time of loss. For older commercial roofs common in established Los Angeles area markets, this depreciation can significantly reduce claim payouts, potentially leaving substantial out-of-pocket costs for property owners.

Functional replacement cost coverage allows insurers to replace damaged roofing with materials that serve the same function but may differ in quality or type from the original installation. This can create complications when dealing with specialized roofing systems or buildings requiring specific performance standards.

California’s unique climate presents specific coverage considerations for commercial properties. Many policies include specific provisions for earthquake damage, requiring separate earthquake insurance for coverage. Additionally, policies may have different deductibles for wind damage versus water damage, impacting how claims are processed and paid.

Understanding your policy’s maintenance requirements is equally important. Most insurers require property owners to maintain roofs in good condition and may deny claims for damage deemed preventable through proper preventive commercial roof maintenance. Regular inspections and documented maintenance become crucial for claim protection.

Essential Documentation for Roof Damage Claims

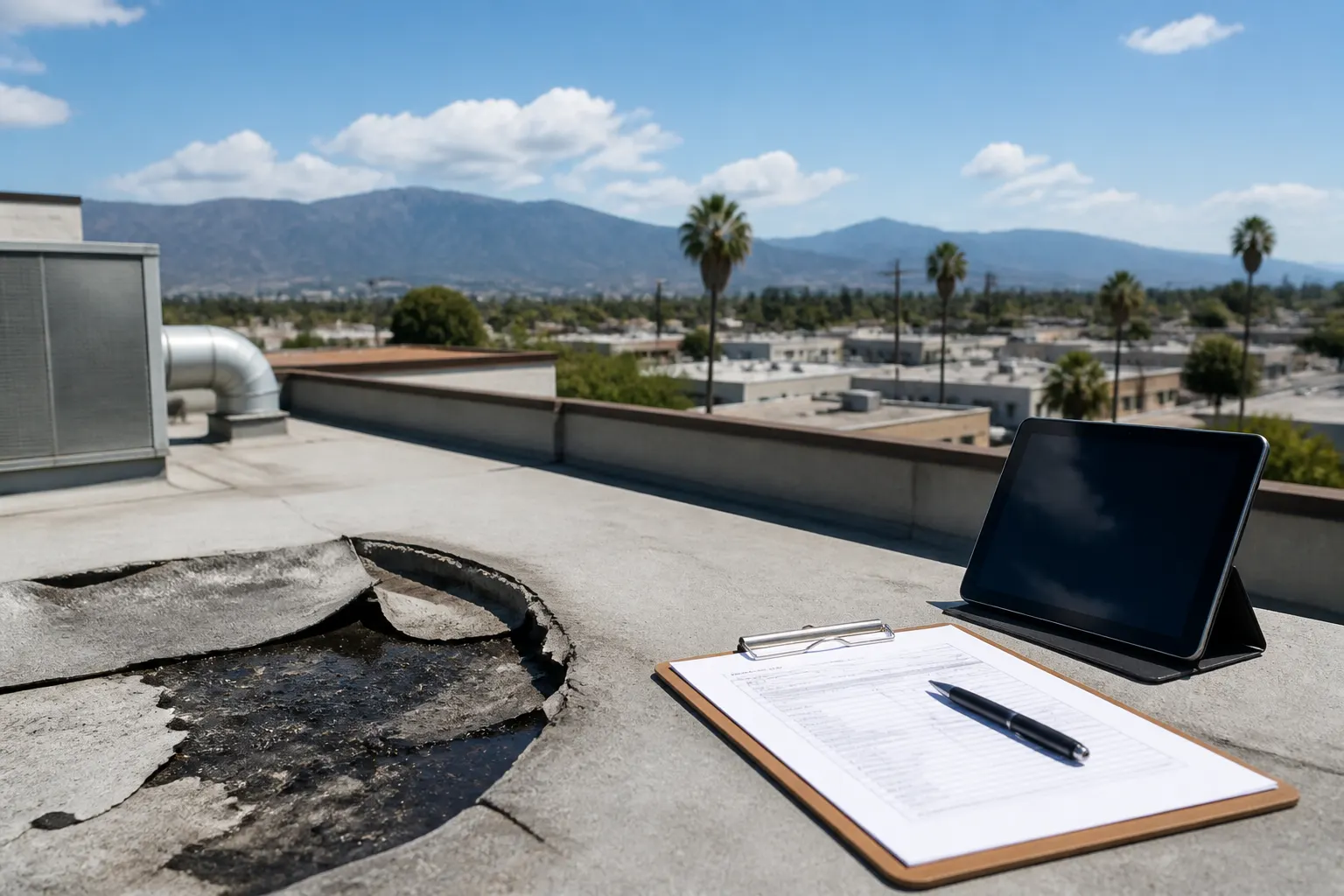

Proper documentation forms the foundation of successful commercial roof insurance claims. The documentation process should begin immediately after discovering damage, before weather conditions worsen or additional damage occurs.

Photographic evidence serves as your primary documentation tool. Capture wide-angle shots showing the overall roof area, then focus on specific damage locations with close-up details. Include reference objects like measuring tapes or coins to show scale. Document the damage from multiple angles, including interior shots if water intrusion has occurred.

Take photographs of the surrounding area to establish context for the damage source. If storm damage occurred, photograph debris, damaged trees, or other evidence of severe weather. For facilities requiring compliance documentation, ensure photos meet your internal documentation standards for incident reporting.

Weather documentation supports your claim by establishing the cause of damage. Obtain official weather reports from the National Weather Service for the damage date, including wind speeds, precipitation amounts, and any severe weather warnings. This documentation proves external forces caused the damage rather than normal wear and deterioration.

Maintenance records demonstrate proper care of your roofing system prior to the damage event. Compile recent inspection reports, maintenance invoices, warranty documentation, and any previous repair records. Well-maintained documentation helps counter potential insurer arguments about pre-existing conditions or neglect.

For healthcare facilities and other regulated properties in Alhambra, CA and throughout Los Angeles County, additional compliance documentation may be required. This includes environmental impact assessments if hazardous materials might be involved, operational continuity plans, and regulatory notification records if damage affects critical systems.

Professional assessments from qualified roofing contractors provide technical documentation insurers require for claim evaluation. Obtain detailed written assessments that specify damage locations, probable causes, and recommended repairs. These assessments should include material specifications and labor requirements for accurate claim valuation.

Create a comprehensive damage inventory listing all affected roof areas, equipment, and interior spaces. Include model numbers, installation dates, and replacement costs for damaged equipment like HVAC units or rooftop equipment. This inventory becomes crucial for ensuring complete claim coverage.

Working Effectively with Insurance Adjusters

The insurance adjuster relationship significantly impacts your claim outcome, making professional collaboration essential for successful resolution. Understanding adjusters’ priorities and constraints helps facilitate productive interactions throughout the claims process.

Initial adjuster contact typically occurs within 24-48 hours of filing your claim. Be prepared to provide basic damage information, policy details, and access arrangements for the adjuster’s inspection. Schedule the inspection promptly, as delays can complicate damage assessment if weather conditions change or additional damage occurs.

Preparation for the adjuster visit should include organizing all documentation, clearing access routes to damaged areas, and ensuring safety measures are in place for roof access. If your facility has specific security or safety protocols, communicate these requirements when scheduling the inspection.

Present documentation systematically during the adjuster meeting. Begin with an overview of your property and roofing system, then walk through the damage chronologically from discovery to current status. Provide copies of all relevant documentation while retaining originals for your records.

Professional contractor involvement during adjuster inspections can significantly improve claim outcomes. Qualified roofing professionals understand technical aspects adjusters evaluate and can identify damage that property managers might overlook. They can also provide on-the-spot technical explanations and repair recommendations.

Contractors experienced with commercial roof repair services in Los Angeles County understand local building codes and typical construction methods, helping adjusters accurately assess repair requirements and costs. However, avoid contractors who guarantee claim approval or offer to work directly with adjusters on pricing - these arrangements often create ethical concerns and can complicate your claim.

Documentation of adjuster meetings protects your interests throughout the process. Take notes during discussions, photograph areas the adjuster examines, and request copies of any measurements or damage assessments they complete. Follow up adjuster visits with written summaries of discussions and agreements reached.

Disagreements with adjusters occasionally arise over damage scope, causes, or repair costs. Address disagreements professionally and promptly, providing additional documentation or expert opinions as needed. Most insurance companies have internal appeal processes for disputed claims that can resolve conflicts without legal intervention.

Navigating the Claims Process Timeline

Commercial roof insurance claims follow predictable timelines, though complex damage or disputes can extend the process significantly. Understanding typical timeframes helps property managers plan accordingly and identify when professional advocacy might be necessary.

Initial claim filing should occur immediately upon damage discovery, typically within 24-48 hours. Most insurers offer 24/7 claim reporting through phone lines or online portals. Provide basic damage information, policy numbers, and contact details, but avoid detailed damage assessments until professional evaluation occurs.

Adjuster assignment and initial contact usually happens within 1-3 business days of filing. California regulations require insurers to acknowledge claims promptly and begin investigations within reasonable timeframes. Document all communication timing for potential regulatory complaints if delays occur.

Property inspection scheduling typically occurs within 5-10 business days of claim filing, though catastrophic events affecting multiple properties can extend this timeline. Emergency repairs to prevent additional damage should proceed immediately, with proper documentation and pre-approval when possible.

Damage assessment completion by the adjuster usually takes 2-4 weeks from the inspection date, depending on damage complexity and contractor estimates required. Simple repairs may be assessed quickly, while complex damage requiring engineering evaluation or specialized contractor input extends the timeline.

Initial settlement offers generally arrive 30-45 days from claim filing for straightforward cases. Complex claims involving multiple building systems, environmental concerns, or coverage disputes can take 60-90 days or longer for initial offers.

Property owners in regulated industries often face additional timeline pressures due to operational requirements. Healthcare facilities, food processing plants, and other compliance-sensitive operations may need expedited repairs to maintain regulatory standing, creating tension with typical insurance timelines.

Emergency repair considerations balance immediate property protection with claim preservation. Most policies require policyholders to prevent additional damage but also require pre-approval for major repairs. Document emergency repairs thoroughly and obtain insurer approval when practical without compromising property protection.

For facilities requiring continuous operations, develop contingency plans that accommodate typical claim timelines. Consider temporary protective measures, alternative operational spaces, or equipment relocation options that maintain compliance while allowing proper claim processing.

Common Coverage Scenarios and Realistic Outcomes

Understanding typical commercial roof damage scenarios helps property managers set realistic expectations and prepare appropriate documentation for their specific situation. Los Angeles area properties face distinct risks requiring targeted preparation strategies.

Storm damage represents the most common commercial roof insurance claim in Southern California. High winds, hail, and heavy rains can damage membrane systems, metal roofing, and rooftop equipment. Coverage typically includes direct storm damage but may exclude flood damage requiring separate coverage.

Wind damage claims often involve membrane punctures, seam failures, or debris impact damage. Well-documented commercial roof maintenance records help establish that damage resulted from storm forces rather than pre-existing deterioration. Insurers typically cover repairs to restore the roof to pre-loss condition using comparable materials.

Age and wear considerations significantly impact claim outcomes for older commercial roofing systems. Insurers may apply depreciation factors or deny claims for damage attributed to normal wear and tear. Properties with roofing systems over 15-20 years old often face increased scrutiny during claim evaluation.

Water damage complications arise when roof leaks cause interior damage to building contents, equipment, or operations. Coverage for consequential damages depends on policy terms and may include business interruption benefits for operational losses. Document interior damage promptly and separate water-damaged contents to prevent mold growth.

Code upgrade requirements can significantly increase claim costs when repairs must meet current building codes that differ from original construction standards. Some policies include ordinance or law coverage for these additional costs, while others exclude code upgrade expenses. California’s evolving energy efficiency requirements under Title-24 may require upgraded materials during repairs.

Partial vs. total roof replacement decisions often create coverage disputes. Insurers prefer partial repairs when possible, while property owners may advocate for complete replacement when damage affects multiple areas or when repairs would create a patchwork appearance. Age, condition, and availability of matching materials influence these decisions.

Temporary protection costs during repairs are typically covered but may be subject to limits or time restrictions. Document temporary protection expenses and coordinate with contractors to minimize these costs while maintaining property protection.

Property managers should understand that insurance companies aim to restore properties to pre-loss condition, not to upgrade or improve them. However, when repairs require current code compliance or when matching materials are unavailable, policies may cover necessary upgrades.

What Contractors Can and Cannot Guarantee About Insurance Claims

Professional roofing contractors play important roles in the insurance claims process, but property managers must understand the limitations of contractor involvement to avoid complications that could jeopardize claim approval or create ethical concerns.

Legitimate contractor services include damage assessment, repair estimates, technical consultation during adjuster meetings, and professional repair work once claims are approved. Qualified contractors provide valuable expertise in identifying damage scope, estimating repair costs, and ensuring repairs meet building codes and manufacturer requirements.

Contractors experienced with California commercial roofing understand local climate challenges, building codes, and typical construction methods. This knowledge helps them provide accurate assessments that align with adjuster expectations and ensure repairs address underlying issues rather than just surface damage.

Prohibited contractor practices include guaranteeing claim approval, offering to waive deductibles, or agreeing to accept whatever insurance pays regardless of actual costs. These practices violate insurance regulations and can result in claim denial or fraud allegations that damage property owners.

Contractors cannot ethically negotiate directly with insurance companies on pricing or coverage decisions. While they can provide technical information and answer questions during adjuster visits, the financial relationship must remain between the property owner and insurer.

Red flags in contractor relationships include door-to-door solicitation immediately after storms, requests for full payment upfront, or suggestions to file claims for damage that may not exist. Reputable contractors focus on legitimate damage assessment and quality repairs rather than maximizing claim amounts through questionable practices.

Property managers should verify contractor licensing through the California Contractors State License Board (CSLB) and confirm insurance coverage before allowing roof access. Licensed commercial roofing contractors in California must maintain proper insurance and bonding to protect property owners during repair work.

Documentation responsibilities remain with property owners even when working with contractors. While contractors can help organize technical information and provide professional assessments, property managers must maintain control over all communication with insurers and claim documentation.

Repair quality standards should meet or exceed pre-loss conditions while complying with current building codes. Contractors should provide warranties on repair work and use materials compatible with existing roofing systems. For facilities in Alhambra, CA requiring specific performance standards, ensure contractors understand compliance requirements before beginning work.

Professional contractors can expedite claims by providing prompt, accurate assessments and maintaining availability for adjuster questions. However, the most valuable contractor services focus on quality repairs that restore property protection rather than manipulating the claims process for maximum payouts.

Conclusion: Protecting Your Investment Through Proper Claims Management

Successfully navigating commercial roof insurance claims requires systematic preparation, thorough documentation, and professional collaboration with qualified contractors and adjusters. Property managers who understand the process, maintain detailed maintenance records, and work with reputable contractors achieve better claim outcomes while minimizing operational disruption.

The key to successful claims lies in preparation before damage occurs. Develop relationships with qualified contractors, understand your policy coverage and limitations, and establish documentation procedures that support future claims. Regular maintenance and inspection not only prevent many damage scenarios but also provide crucial documentation supporting claim legitimacy.

For facilities requiring regulatory compliance, integrate insurance claims procedures into your overall risk management and operational continuity planning. Understanding typical claim timelines helps maintain compliance while allowing proper claim processing.

When roof damage affects your commercial property, don’t navigate the complex claims process alone. Contact HP Roofing Pro today for professional damage assessment, technical expertise during adjuster meetings, and quality repairs that restore your property protection while meeting all insurance and regulatory requirements. Our experienced team understands both the technical aspects of commercial roofing and the documentation needs of successful insurance claims, helping Los Angeles area property managers protect their investments and maintain operational continuity.